S&P recently showed the results of its latest survey, according to which risk appetite went from a sharp increase to a decrease in a short period of time. And now there is such risk appetite for, let’s say, crippling equations. Overall, its long-term development could be based on a simple balance between the evolution of the macroeconomic environment. Just don’t sit here. Today, a technique on the dark side of risk and what investors demand for it.

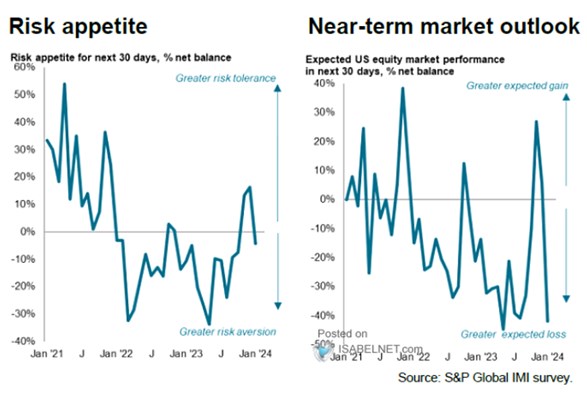

1. For two years the attitude towards risk was negative, now almost neutral: the results of the evolution of the survey are summarized in the following two graphs. In the second there is a specific vision of the short-term performance of the stock markets, in the first there is an aversion, even a tendency towards risk. It was supposed to be quite high in 2021, but then, according to the chart, it started to fall and gradually turned into a notable aversion. It started to decline around the middle of last year, and the current one is that the local peak turns into water:

Source: X

Over the course of 2021, we have begun to show more and more how relative the word pedestrian is. That is, inflationary pressures have a profound end, which is not expected. And so the Fed finally started to sharply raise rates at its 2022 meeting. This was around the time when the possibility for further development was well developed, macro uncertainty was high, and the development described in the first chart would correspond well to a high risk aversion. In 2023, inflation began to trend downward again, and here the situation began to calm down and the monetary policy path began to become clearer (compared to what was open before). And risk aversion was waning.

2. But this indicates many lows: Now the situation described in the first graph is in the middle, somewhere on the neutral line. And the graph, from my point of view, would approximately correspond to the general environment. But I wrote in the water that there is something wrong here, namely the discrepancy between the first graph and the development of the risk lines on the stock market. These should reflect risk aversion/appetite, but cannot be observed. There are their mountain estimates and lep estimates (see also no). Among these types, perhaps five are those of Goldman Sachs, which I have briefly shown here:

Source: X

According to these estimates, risk premiums in the United States and around the world rose sharply in the first half of 2020, then trended downwards and stood at the same level as the last ten years in the autumn. Especially in the USA there is no real growth due to the fluctuating inflation and monetary equivalent of previous years. And while according to the aforementioned survey the current attitude of investors towards risk is almost neutral, according to their estimates investors are particularly risk averse.

3. Explained? People can cut something else (first graph) and cut something else (straight line). They are the first prizes that are not based on this macroeconomic trend. It is therefore possible that Goldman Sachs’ methodology is also not completely complete. That is, it does not lead to the estimation of fees.

In a certain sense it is better to mix the straight line and the expected growth, which we arrive at if we subtract the risk-free rate from the inverse PE. The result of urits is not simply a straight line, as some claim (and here the result should not be used by you to estimate the value of some companies). It is a kind of indicator of general optimism, which includes both average and expected growth in profits and dividends. And it is quite easy to imagine that this general optimism did not really survive the arc of macroeconomic development, because the growth rate (related to artificial intelligence) was probably outside the direct costs themselves. So he provided an example of how busy markets are now with new technologies.

Patria.cz is Patria Finance’s investment portal with real-time data on domestic and foreign capital markets. We provide online information and analytical support in the fields of finance, macroeconomics and investments. Of course, current investment advice and long-term investments are recommended. Stocks, currencies, commodities, recommended investments: at a glance in one place.

2024-01-19 16:16:00

#Nco #doesnt #play #Kurzy.cz